.jpg")

After the Brexit, the trade of goods with or within the EU has changed drastically for many of the UK businesses. Suddenly all the B2B trade that could be normally subject to zero VAT, is now involving registering for VAT number and paying VAT. Moreover, some of the special simplified tax schemes are not so easy to be used. Nevertheless, it might still be possible, let’s take a look how the triangulation simplification could be applied.

Can I use the triangulation simplification?

Should your company purchase the goods from one European country, and afterwards supply these goods directly to the final business customer, established in another EU country, other than your own, your company may profit from a simplification regime, allowing not to register for VAT purposes in the final country of arrival. Moreover, in this type of supply, all parties can apply a zero VAT rate. This is a simplification mode called ‘VAT triangulation scheme’ offered by EU regulation to simplify trade between different businesses established in the EU.

May sound a bit confusing, let’s look at it visually:

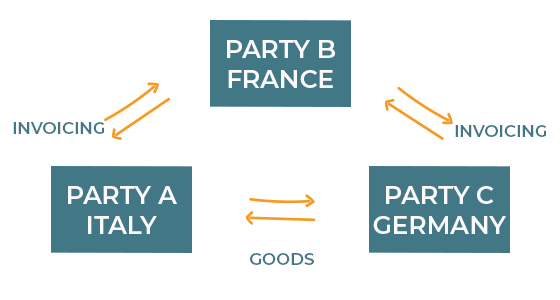

EXAMPLE

Transaction

Let’s say Company B established in France is purchasing goods from Company A established in Italy and afterwards sell them to Company C which is established in Germany. The goods in question are held in Italy by Company A at the beginning of the transaction, and are shipped directly to Company C to Germany, without passing through France.

Now it is clear why it is called triangulation! Indeed, the easiest way to visualize the scheme is to draw an imaginary triangle.

VAT & Intrastat reporting

Further, how this transaction would look like from a VAT point of view? Basically, there are two Intra Community supplies, however, they are not connected with the real movement of the goods. Let’s see how each of the parties will have to report the transaction on their VAT reporting.

Reporting 1 Company A in Italy:

- VAT return in Italy – Intra Community Supply to be reported

- Intrastat in Italy – dispatches to be reported

Reporting 2 Company B in France:

- VAT return in France – no Intra Community acquisition to be reported! Only Intra Community Supply to be reported

- Intrastat – dispatches (with DE VAT number of Company C)

Reporting 3 Company C in Germany:

- VAT return in Germany – Intra Community Acquisition to be reported

- Intrastat in Germany – arrivals to be reported (with the country of dispatch being Italy)

How do I profit from the triangulation scheme after the Brexit?

After the Brexit, many companies, that were used to the simple and convenient way of reporting their intra EU B2B trade, suddenly were left without a solution. Indeed, as UK is not part of the EU anymore, the company’s UK VAT number cannot be used in the triangulation scheme and therefore, multiple VAT liabilities arise for your company.

Solution may be to have at least one VAT number in the EU, which would allow the trade between different EU countries under the existing triangulation scheme. However, be careful, as your customer will need to have the VAT registration in the country of arrival! Therefore, it is advised to first check whether all the conditions of triangulation are fulfilled before proceeding with the application of zero VAT rate.

Eurotax’s team of experts will gladly review your flows and confirm how to correctly apply the simplification mechanisms of European VAT. You can contact us here.